.png)

Pet Grooming Business Insurance Guide

Protect your grooming business with the right insurance. Learn coverage all pet groomer needs

One dog bite. One slip on a wet floor. One allergic reaction to shampoo. Any of these could cost you thousands—or end your grooming business entirely. Pet grooming business insurance isn’t optional; it’s essential protection for your livelihood.

This guide explains the coverage you need, what it costs, and how to choose the right insurance for your grooming business.

Why Groomers Need Insurance

The Risks Are Real

Pet grooming involves inherent risks.

Injury to animals

- Clipper cuts and nicks

- Burns from dryers

- Falls from tables

- Allergic reactions

- Stress-related incidents

- Escapes and runaways

Injury to people

- Dog bites to you or clients

- Slip-and-fall accidents

- Allergic reactions

- Vehicle accidents (mobile groomers)

Property damage

- Damage to client property

- Fire or water damage to your space

- Vehicle damage

- Equipment theft or damage

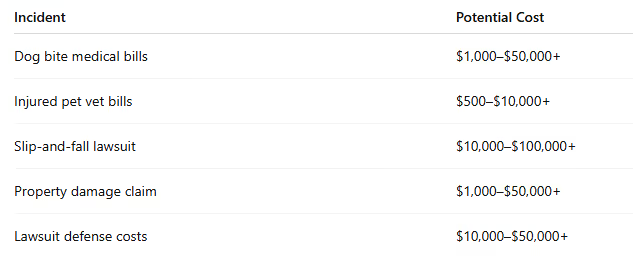

The Financial Impact

Without insurance, one incident could bankrupt your business.

Essential Insurance Types for Groomers

1. General Liability Insurance

What it covers

- Bodily injury to third parties (clients, visitors)

- Property damage you cause

- Personal injury (slander, libel)

- Medical payments for injuries at your location

- Legal defense costs

Example scenarios

- A client trips over equipment in your salon

- Client property is damaged during an appointment

- Someone is injured by a dog in your care

Typical coverage: $1–2 million per occurrence / $2–4 million aggregate

Typical cost: $400–$1,200 per year

2. Professional Liability (Errors & Omissions)

What it covers

- Injury to animals in your care

- Negligence claims related to grooming services

- Errors in service that cause harm

- Defense costs for grooming-related lawsuits

Example scenarios

- Dog develops skin irritation after grooming

- Pet is injured during grooming

- Animal escapes and is lost or hurt

- Clipper burn or cut requiring veterinary care

Why general liability isn’t enough

General liability covers third-party injury and property damage. Professional liability covers harm resulting from your professional services—critical for animal care businesses.

Typical coverage: $500,000–$2 million

Typical cost: $300–$800 per year

3. Business Property Insurance

What it covers

- Grooming equipment (clippers, dryers, tables)

- Supplies and inventory

- Furniture and fixtures

- Business records and documents

- Signage

Example scenarios

- Fire damages grooming equipment

- Theft of tools

- Water damage to supplies

Typical coverage: Replacement value of assets

Typical cost: $200–$800 per year

4. Business Owner’s Policy (BOP)

A BOP bundles multiple coverages at a discount.

Typically includes

- General liability

- Business property

- Business interruption

Advantages

- Simpler than multiple policies

- Usually cheaper than buying separately

- Single renewal

Typical cost: $500–$1,500 per year

Note: Most BOPs do not include professional liability, which is usually purchased separately.

5. Commercial Auto Insurance (Mobile Groomers)

What it covers

- Liability for vehicle accidents

- Vehicle damage

- Medical payments

- Uninsured motorist coverage

- Equipment inside the vehicle

Required for mobile groomers. Personal auto insurance usually excludes commercial use.

Typical cost: $2,000–$5,000 per year

6. Workers’ Compensation

What it covers

- Medical expenses for work-related injuries

- Lost wages

- Disability benefits

- Rehabilitation costs

Required in most states if you have employees.

Typical cost: $0.50–$2.00 per $100 of payroll

7. Optional and Specialty Coverage

Care, Custody, and Control (CCC)

Covers animals in your care if excluded from general liability.

Inland Marine

Covers equipment in transit (important for mobile groomers).

Cyber Liability

Protects against data breaches involving client information.

Employment Practices Liability

Covers employee-related claims such as discrimination or wrongful termination.

Insurance Requirements by Business Type

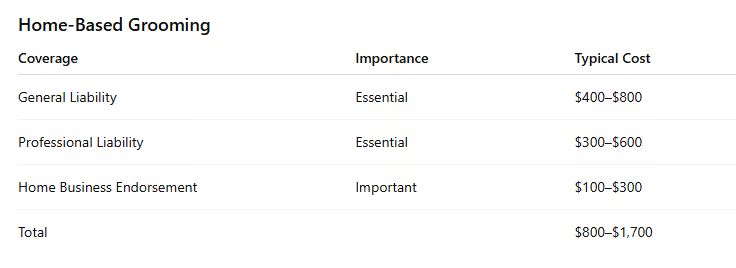

Home-Based Grooming

Homeowners insurance usually excludes business activities.

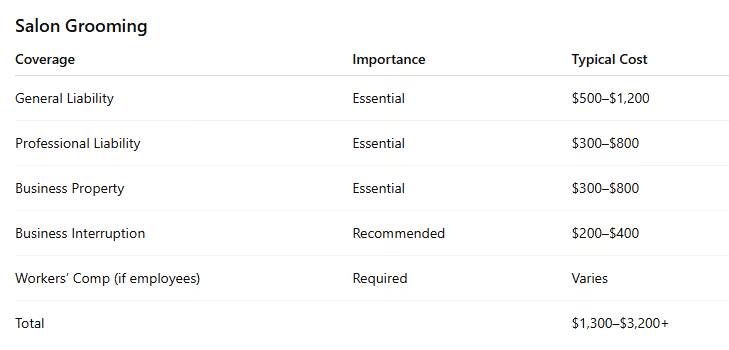

Salon Grooming

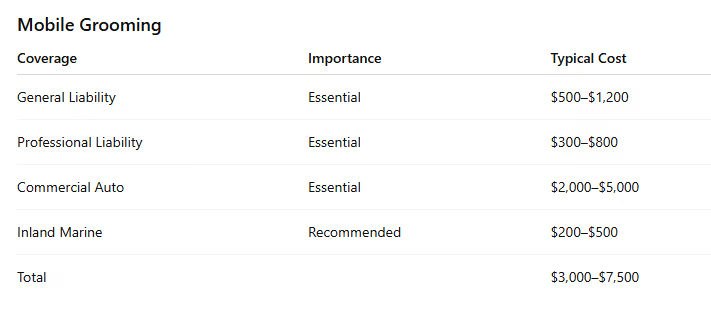

Mobile Grooming

How Much Does Groomer Insurance Cost?

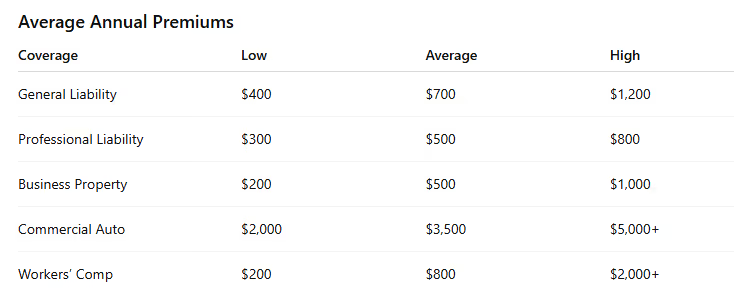

Average Annual Premiums

Factors That Affect Your Premium

Higher premiums

- More employees

- Higher revenue

- Claims history

- High-risk breeds

- Mobile operations

- Expensive equipment

Lower premiums

- Solo operation

- Lower revenue

- Clean claims history

- Safety certifications

- Home-based business

- Higher deductibles

Ways to Reduce Costs

- Bundle policies

- Increase deductibles

- Obtain certifications

- Maintain clean claims records

- Shop around

- Pay annually

How to Get Insurance

Step 1: Assess Your Needs

Consider business type, employees, equipment value, revenue, and risk tolerance.

Step 2: Shop Multiple Quotes

Compare specialty pet insurers, general business insurers, brokers, and professional associations.

Step 3: Compare Coverage, Not Just Price

Review limits, deductibles, exclusions, claims process, and insurer stability.

Step 4: Ask Questions

Confirm animal coverage, exclusions, claim procedures, and coverage caps.

Step 5: Review Annually

Adjust coverage as your business grows or changes.

Understanding Your Policy

Key terms

- Premium

- Deductible

- Coverage limit

- Per occurrence

- Aggregate

- Exclusion

- Endorsement

Common exclusions

- Intentional acts

- Your own animals

- Pre-existing conditions

- Certain breeds

- Criminal acts

- Transport damage without commercial auto

- Employees without workers’ comp

What to Do When an Incident Occurs

Immediate steps

- Ensure safety

- Document everything

- Collect witness information

- Provide first aid if qualified

- Seek medical or veterinary care

- Do not admit fault

Reporting

- Report promptly

- Provide full documentation

- Keep copies

Minimizing Risk (and Premiums)

- Proper restraints and non-slip mats

- Regular equipment maintenance

- Dryer temperature monitoring

- Clear procedures for aggressive animals

- Thorough documentation

- Staff training and first aid certification

Final Thoughts

Insurance isn’t the most exciting part of running a grooming business, but it’s one of the most important. One uninsured incident could cost you everything you’ve built.

Carry the right coverage. Review it yearly. Protect your business.

Peace of mind is worth every penny.

![Teddy vs Gingr: Complete Comparison [2026]](https://cdn.prod.website-files.com/64ac1f211014e9b293d35a4a/698dede605a81497c71168d0_Teddy%20vs%20Gingr_%20Complete%20Comparison%20%5B2026%5D.png)